Public Pensions

The City participates as one of more than 935 plans in the defined benefit cash-balance plan administered by TMRS. TMRS is a statewide public retirement plan created by the State of Texas and administered in accordance with the Texas Government Code, Subtitle G, Title 8 (TMRS Act) as an agent multiple-employer retirement system for employees of Texas participating cities. The TMRS Act places the general administration and management of TMRS with a six-member, Governor-appointed Board of Trustees; however, TMRS is not fiscally dependent on the State of Texas. TMRS issues a publicly available Annual Comprehensive Financial Report (ACFR) that can be obtained at www.tmrs.com.

All eligible employees of the City are required to participate in TMRS. Upon retirement, the employee account balance including interest is combined with the employer match to price a lifetime annuity based on the employee’s age at retirement.

Benefits Provided

Round Rock has chosen from a menu of plan options as authorized by the TMRS statute. Round Rock’s plan provides the following benefit level:

Employee Contributions: 7% of pay

City to Employee Matching Ratio: 2 to 1

Updated Service Credit Rate: 100% repeating transfers

Cost of Living Adjustments: 70% of CPI repeating

Years Required for Vesting: 5

Service Retirement Eligibility: 20 years at any age, vested and age 60

Supplemental Death Benefit to Active Employees: Yes

Supplemental Death Benefit to Retirees: Yes

Employees Covered by Benefit Terms

At the December 31, 2024 valuation and measurement date, the following employees were covered by the benefit terms:

Inactive employees or beneficiaries currently receiving benefits 522

Inactive employees entitled to but not yet receiving benefits 630

Active employees 1,166

Total 2,318

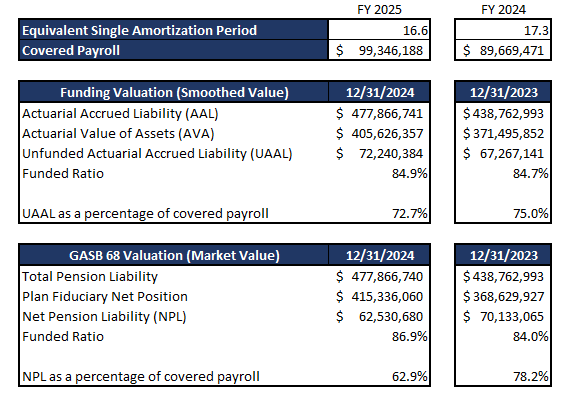

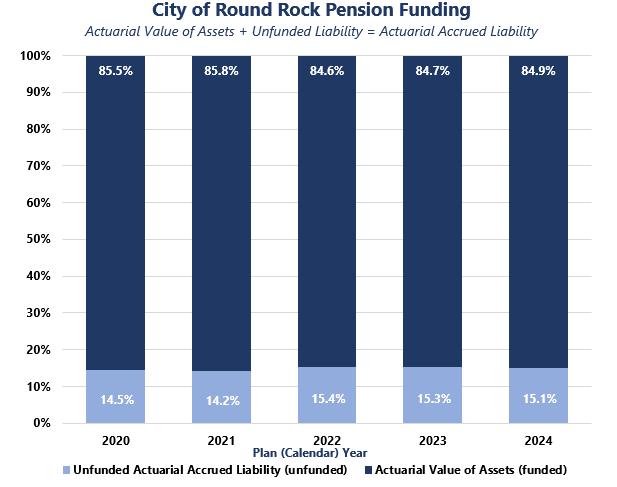

Pension Summary

TMRS provides each of its member cities with two slightly different actuarial valuations which are both reflected below as of December 31, 2024 (TMRS’ year-end is December 31, 2024, and that is the most recent valuation date for which data is available and has been provided to the City). The first is a funding valuation which uses a smoothed actuarial value of assets to calculate the City of Round Rock’s actuarially determined contribution (ADC) to the plan. The second valuation is provided for Governmental Accounting Standards Board (GASB) Pronouncement 68 financial reporting purposes and reflects the City of Round Rock’s fiduciary net position based on the market value of its assets on the reporting date. Results of the most recent valuation follows:

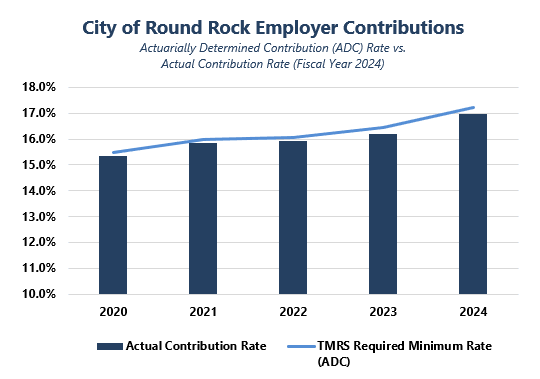

Using both valuation methods, the City’s funded ratio is above 80%. It is important to note that the primary financial objective of TMRS is to achieve the long-term full funding of promised benefits and each calendar year, TMRS informs the City of what its contribution requirements are to achieve this financial objective.

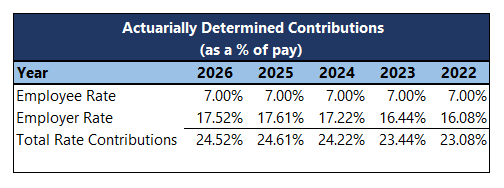

Contributions

Employees are required to contribute 7% of their annual gross earnings based on the City’s plan provisions.

Investments

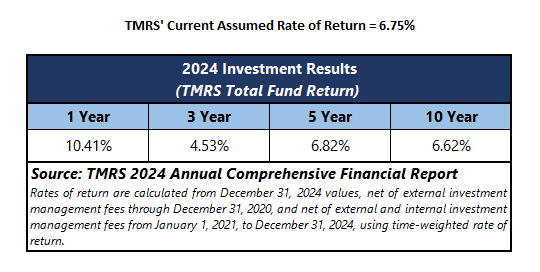

More detailed information regarding investment objectives, policies, and performance of the TMRS pension system can be found at www.tmrs.com or in the TMRS Annual Financial Report. TMRS’ current assumed rate of return and total fund return at 1 year, 3 years, 5 years, and 10 years, follow:

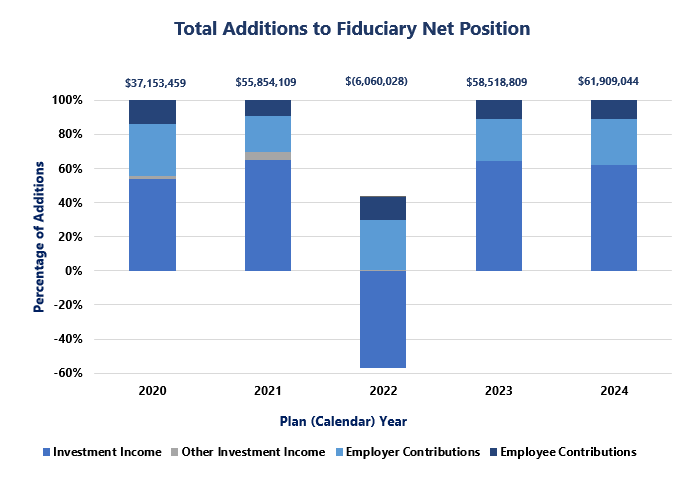

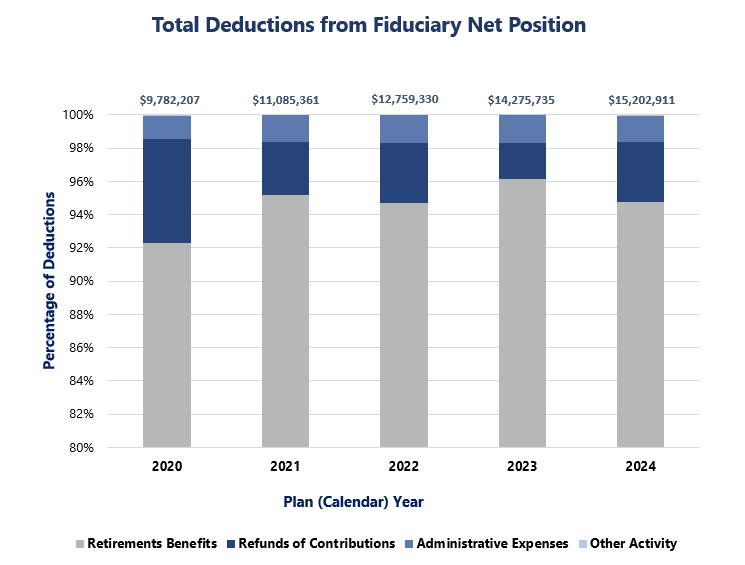

Changes in Fiduciary Net Position

The fiduciary net position is the market value of the assets of the trust. For GASB 68 reporting purposes, the City of Round Rock’s total pension liability is reduced by the fiduciary net position to arrive at the City’s net pension liability. The breakout of the additions to and deductions from the City’s fiduciary net position for the most recent valuation period as of December 31, 2024, follows:

As of December 31, 2024, TMRS exceeded the assumed interest rate of return of 6.75% with an investment return of 10.41%. This, in turn, resulted in a net decrease of $7,602,385 in the City’s net pension liability. TMRS is a long-term investor; portfolio diversification helps mitigate losses over time and actuarial smoothing of assets reduces the contribution rate volatility that would otherwise be associated with gains and losses based on a single year’s investment performance.

Total Deductions from Fiduciary Net Positions.

Reference Documents and Schedules

- FY2024 Schedule of Changes in Fiduciary Net Position (Pages 40-41)

- FY2023 Schedule of Changes in Fiduciary Net Position (Pages 40-41)

- FY2022 Schedule of Changes in Fiduciary Net Position (Pages 40-41)

- FY2021 Schedule of Changes in Fiduciary Net Position (Pages 48-49)

- FY2020 Schedule of Changes in Fiduciary Net Position (Pages 40-41)